Date Posted: November 16th, 2017

Game on: the potential for gamification in asset management

Millennials, whether fair or not, do not have a great reputation. This group of people, born sometime between 1980 and 2000 are according to some lazy, entitled, narcissistic and more interested in their smartphones than human interaction. Yet, others praise their work ethic and argue that businesses need to recognise their potential.

Mixed perceptions of this ‘Me Me Me Generation’ continue when it comes to their finances. According to a recent report by Merrill Edge, millennials are saving but for different reasons than their parents. They save to live their desired lifestyle rather than to leave the workforce. They are less interested in getting married and becoming parents than older generations, but more desirous of working their dream job and travelling the world.

Financial expectations are changing. For millennial’s short-term goals are much more important than worrying about the future. This goes some way to explaining why they are good at saving but not so interested in investing. For many, growing up during the Financial Crisis and seeing their parents suffer, has engendered significant distrust in investments, big corporations and risk more generally.

Relatability is another issue. The investment industry is not considered ’hip’ and as such, many young people fail to connect to the industry.

This wariness of investing is compounded by high student debt, house price rises and the fact that young adults today earn significantly less than their counterparts in past decades.

Not just a millennial problem

So, what does this mean for asset managers and the savings vehicles that support them? While millennial saving for short term goals may be damaging to their long term financial health, it is also bad news for asset managers. Without the custom of the incoming generation, the industry will face some serious challenges. Recent research from Wealth-X found that 81% of asset managers say they want to become more attractive to the younger generation, so many are acutely aware of the issue and are making it a focus. Yet, we are not seeing much real-life evidence in terms of a shift.

It’s simple – asset managers that fail to adapt business and operating models to attract the next generation of wealth may risk losing a substantial pool of future investments. It is essential that we work together to harness the upcoming generation by showcasing the potential success of investing.

It’s game time

The big question is how?

Gamification, defined as “the process of adding games or gamelike elements to something (such as a task) so as to encourage participation” may be one way to engage and educate future investors.

The principles of gamification have been used successfully in a range of scenarios. Although many of us would not consider ourselves ‘gamers,’ we have probably encountered gamification techniques in various guises throughout our daily lives; from walking that bit further to reach our Fitbit reward to moving up levels on retail or airline loyalty programs.

Gamification principles are not restricted to recreational activities; tangible business problems have also been tackled using this approach including improving security awareness (by improving employees’ filtering of phishing emails) and enhancing stakeholder engagement (by facilitating ‘tailored story-telling’ by external stakeholders and employees as they explore the firm’s vision and culture platform). But, how does this relate to personal investing? What specific techniques can individuals adopt to make long-term saving more appealing to the younger generation?

The potential impact of gamification

Encourage investment

To attract millennials, you must be able to demonstrate the potential reward as well as the risks of investing. For example, allowing potential investors to learn about investing through fun, game-like processes rather than overwhelming them with technical requirements and phrases. There is a knowledge gap when it comes to financial terminology, especially amongst young people, so any communication must be simple and relatable. Once they feel confident, they can then transition to trading real stocks.

By providing first time investors with no-risk educational tools prior to making real investment decisions, asset managers could encourage participation amongst this generation of historically cautious investors. Better education can also improve investment strategies and outcomes, all of which improves asset manager profitability.

Assess risk and reinforce positive behaviour

Although many millennials are conservative, they are not completely immune to risk. However, in an age where lives can be managed on smart phones, few younger investors appreciate filling in lengthy risk appetite questionnaires. This is one area where gamification could not only vastly improve engagement, but also the accuracy of outcomes.

Current questionnaires can be flawed and rely on individuals understanding their own inherent biases and motivations which paves the way for inaccuracy. In comparison, games can be instinctive, simpler and better at simulating real life experiences. Furthermore, they can be repeated with higher frequency and ease than questionnaires.

Moving to an online platform, where decisions can be made online, alongside a progress tracker, to identify what other decisions can be made, helps users understand their options.

Pic 2: progress tracker

In a gamified setting, this could allow for the reinforcement of positive behaviour through rewards, improving outcomes for both the investor and manager in the long term.

Improve customer retention

Investment startups using gamification techniques don’t just aim to improve trust and education in the investment process, they also want to make it fun – an adjective perhaps not always associated with investment processes of old.

Investing real money is of course not a game in itself, and sensible risk taking should always be prioritised above simply ‘having fun.’ However, the two need not be mutually exclusive. By continuously engaging with customers in a manner that is both fun but also demonstrates an understanding of their goals and concerns, asset managers can increase loyalty amongst a generation known for its lack of brand allegiance.

Looking at pensions

Defined Contribution pension schemes are a perfect example of a long-term savings vehicle that many people have by default, but could benefit from gamification to help younger individuals understand what they will get in return for their savings. There is a general mentality, particularly for millennials, that it is all so far away and something for other people to worry about. However, everyone gets old and knows someone who is retired or nearing retirement, so whilst they might not ‘get’ the idea of saving an amount for some remote future, they definitely don’t want to work forever.

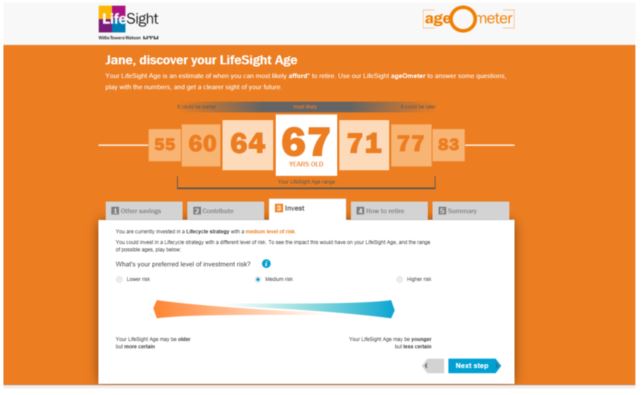

Most will be intrigued about when they are likely to be able to down tools, so it is important to give individuals access to personalised tools to help bring this to life. For example, a tool which gives all members a result with a human metric that everyone can understand. The metric – the age when can you afford to retire – can be made more accurate and personal by inputting more data about past savings and can reflect changes in investment strategy and contributions.

Pic 3: How risk appetite affects the age at which you can afford to retire

We know that helping millennials build a good retirement income is going to be a long and tough road, where we will need to learn about how best to help them on their journey as much as they will need to learn about how best to save for retirement. Understanding what they do on the site and getting feedback from members about what they like and don’t like is integral so that schemes can keep meeting the needs of their members and ensure they have great pension outcomes.

Game on – the wider impact on Asset Managers

Adapting business models to meet the requirements of future investors is not simply a technology bolt-on. To be successful it will also require traditional work and talent structures to change.

Asset managers will need to understand the key role technology has to play in their core business strategy as well as which cultural attributes and organisational capabilities will create competitive advantage in this new landscape. Talent will need to be realigned with these priorities which may require asset managers to look for skills outside of their traditional employee base – from software developers to artificial intelligence.

The potential of gamification is significant when it comes to both raising the profile of a variety of investment options for the younger generation and making them more attractive in the process. Whilst it will require a change of mindset and the introduction of new talent to ensure success, it is an essential step-change to ensure future proof investments and the success of the industry as a whole.